📝 Topics Covered

- 4.1 🛡️ The Core Philosophy of Insurance

- Risk Transfer Mechanics

- Critical Checks (CSR, Claim Amount Ratio, Solvency)

- 4.2 👨👩👧👦 Life Insurance: Protecting Your Dependents

- Term Life vs. Endowment vs. Whole Life vs. ULIPs

- Government Subsidized Life Cover (PMJJBY)

- 4.3 🚑 Health & Personal Accidental Insurance

- Accidental Protection (PMSBY)

- The Ultimate Health Insurance Checklist

- 4.4 📐 Calculating Your Optimum Insurance Cover

- The Income Multiplier Matrix

- 4.5 💳 Hidden / Free Default Insurance Benefits

- Debit Card Insurance (HDFC Millennia Case Study)

- Pradhan Mantri Jan Dhan Yojana (RuPay PMJDY) Free Cover

- 4.6 🧘♂️ Gyan: The Umbrella Metaphor

- Strategic Peace of Mind

4.1 🛡️ The Core Philosophy of Insurance

The life, health, and property of any individual are constantly surrounded by the unpredictable risks of death, illness, severe disability, or accidents. While we cannot prevent misfortune, we can eliminate its catastrophic financial consequences.

Insurance is a prudent financial tool designed to mathematically transfer these high-impact risks from you (the individual) to a large, highly regulated insurance company.

graph LR

User[You / Your Family] -- Pays Premium <br> (Small, Predictable Cost) --> Insurer[Insurance Company]

Insurer -- Bears Financial Risk <br> (Massive Potential Cost) --> User

Critical Quality Checks Before Buying Any Policy

Before selecting an insurance provider, you must rigorously evaluate three foundational financial metrics defined by the regulator (IRDAI):

| Foundational Metric | Meaning & Importance | Target Benchmark |

|---|---|---|

| Claim Settlement Ratio (CSR) | The percentage of total claims received that the company successfully approved and paid out in a year. | > 97% |

| Claim Amount Settlement Ratio | The percentage of total claimed monetary amount paid out. Avoids companies that approve small claims but reject large ones to artificially inflate their CSR. | > 90% |

| Solvency Ratio | The ratio of the insurer’s assets to its liabilities. It measures the company’s financial strength to pay massive claims during extreme black-swan events. | > 1.5 (150%) (Aim for > 1.8) |

4.2 👨👩👧👦 Life Insurance: Protecting Your Dependents

The Golden Rule: You strictly need Life Insurance ONLY if someone is financially dependent on your active income. If no one depends on you, no life insurance is required.

There are four primary vehicles for life insurance in the market. Knowing which one to buy will save you lakhs in wasted premiums:

| Policy Category | Investment / Maturity Value | Strategic Verdict & Purpose |

|---|---|---|

| Pure Term Life Plan 🛡️ | Zero (No Return) | The Ultimate Choice. Extremely cheap, essential, and provides a massive payout to your family strictly in the event of your demise. It separates protection from investment. |

| Endowment Policies 🏢 | Low | Avoid. A deceptive combination of safety and savings. The maturity returns are notoriously low (4-6% p.a.), and the life cover is severely inadequate. |

| Whole Life Policies 👴 | Moderate | You pay premiums for a fixed term and remain covered for your entire life (up to 99 years). Useful only for high-net-worth estate planning. |

| ULIPs (Unit Linked Plans) 📈 | Market-Linked | Avoid. Premiums are invested in the stock market. High front-loaded management fees, administrative charges, and poor flexibility dilute your returns. |

Government Subsidized Life Insurance

For basic financial security, the government offers a highly subsidized life cover program:

- Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY):

- Sum Assured: ₹2 Lakhs

- Eligibility: Age 18 to 50 years with a linked savings account.

- Annual Premium: ₹436/year (subsidized and auto-debited).

4.3 🚑 Health & Personal Accidental Insurance

Personal Accidental Insurance

Accidental insurance is a complementary cover designed to protect your income in the event of physical disability or accidental death.

- Government Scheme: Pradhan Mantri Suraksha Bima Yojana (PMSBY)

- Sum Assured: ₹2 Lakhs

- Annual Premium: ₹20/year (auto-debited).

Health Insurance (HI) 🏥

Health insurance covers medical bills when you are admitted to a hospital for a minimum of 24 hours. A single medical emergency can completely wipe out a lifetime of stock market savings.

The Ultimate Health Insurance Buying Checklist:

- ❌ Room Rent Capping: Ensure the policy has “No Room Rent Capping” or allows a “Single Private A/C Room”. If your room rent is capped (e.g., 1% of sum insured), the hospital proportionately inflates every single charge (doctor visits, surgeries), leaving you with a massive out-of-pocket bill on maturity.

- ⚖️ Co-Payment Clause: Ensure the policy has 0% Co-Payment. Co-payment mandates that you pay a fixed percentage (e.g., 10-20%) of every hospital bill, which defeats the purpose of buying insurance.

- 🔄 Restoration / Recharge Benefit: Look for automatic restoration of the sum insured if you exhaust your coverage during a single year.

- ⏱️ Pre-Existing Disease (PED) Waiting Period: Ensure the waiting period for chronic conditions (like Diabetes or Blood Pressure) is low (ideally 2 to 3 years, rather than 4).

- 🏥 Network Hospital Density: Verify that the insurance company has direct cashless tie-ups with premium hospitals in your immediate geographic vicinity.

💡 Smart Rider Pro-Tip: Always purchase Accidental Disability and Critical Illness as Riders on your core Term Life Insurance rather than adding them to your Health Insurance. Riders on Term Life are significantly cheaper and offer a fixed, tax-free lump-sum payout upon diagnosis!

4.4 📐 Calculating Your Optimum Insurance Cover

Calculating how much coverage you need depends on your age, financial liabilities, and remaining wealth-building years:

$$\text{Minimum Cover} = \text{Current Annual Income} \times 10$$ $$\text{Ideal Cover} = \text{Current Annual Income} \times \text{Age Multiplier} + \text{Total Liabilities (Loans)}$$

The Income Multiplier Matrix

| Current Age | Ideal Cover Multiplier | Example (If Income is ₹10 Lakhs) |

|---|---|---|

| 18 - 35 | Income $\times$ 25 | ₹2.5 Crores |

| 35 - 40 | Income $\times$ 20 | ₹2.0 Crores |

| 40 - 50 | Income $\times$ 15 | ₹1.5 Crores |

| 50 - 60 | Income $\times$ 10 | ₹1.0 Crores |

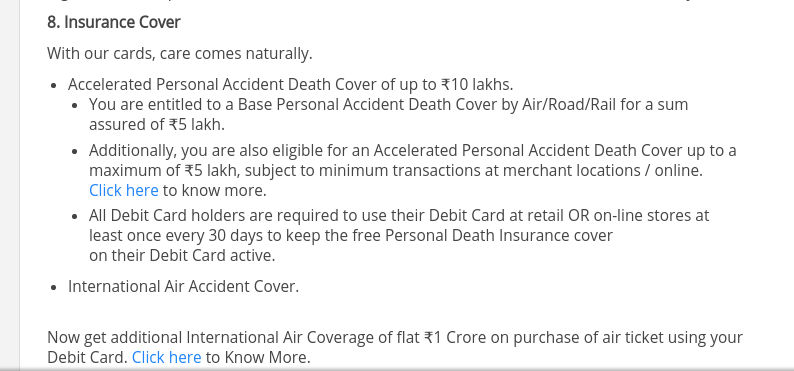

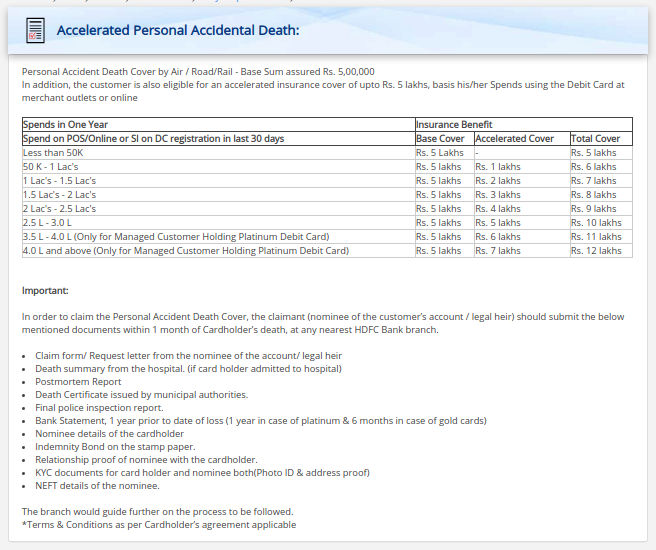

4.5 💳 Hidden / Free Default Insurance Benefits

Many premium debit cards and credit cards silently bundle complimentary accidental death insurance for their cardholders. You pay no premiums, but your nominees are fully protected.

Case Study: HDFC Debit Card Insurance

HDFC Bank provides a free ₹5 Lakh + ₹5 Lakh accidental death cover to active Millennia Debit Card holders.

🏦 RuPay Jan Dhan (PMJDY) Free Insurance

All citizens holding a RuPay Card issued under the Pradhan Mantri Jan Dhan Yojana program possess built-in Accidental Insurance.

| RuPay Policy Type | Issue Date Details | Free Sum Insured |

|---|---|---|

| PMJDY OLD | Accounts issued before 28th Aug 2018 | ₹1 Lakh |

| PMJDY NEW | Accounts issued after 28th Aug 2018 | ₹2 Lakhs |

How to Safely File a Claim:

- Critical Condition: The cardholder must have completed at least one successful financial transaction (ATM, POS, e-com, online) within 90 days prior to the accident date.

- The claim paperwork must be physically submitted within 60 days of the accident.

- Contact the exact bank branch that issued the RuPay card to start the claim.

🎥 RuPay Card Insurance Deep Dive

4.6 🧘♂️ Gyan: The Umbrella Metaphor

Insurance is often misunderstood as an expense or an investment. In reality, it is pure risk management.

“Insurance is like an umbrella. You do not carry it because you hope it rains; you carry it so that when a storm hits, you can continue walking through the rain without getting wet, protecting the loved ones under your shelter.”

🚀 Immediate Action Items:

- Open your net-banking account and search for PMJJBY and PMSBY.

- Seamlessly enroll in both. It takes less than 2 minutes and costs less than a single cup of premium coffee per year (₹456 combined), securing a ₹4 Lakh cover for your family!

Reference

- HDFC Millennia Debit Card Benefits

- HDFC Accelerated Personal Accidental Death Cover

- RuPay PMJDY Cards: Frequently Asked Questions

- Claims Process – RuPay Insurance Program for RuPay PMJDY

- Labour Law Advisor: Free Debit Card Insurance Guide

- Download PMJJBY Certificate (SBI Portal)

- Download PMSBY Certificate (National Insurance Portal)